The Short Answer: Can You Sell During Foreclosure In LA?

Yes, you can usually sell your house while it’s in foreclosure, as long as the home has not been sold at the trustee sale yet. The foreclosure process requires multiple notice steps before an auction can take place, and many homeowners sell during that window.

What determines how easy the sale will be:

- How far along the foreclosure timeline are (Notice of Default vs Notice of Trustee’s Sale)?

- Whether you have equity (sale price can cover the loan payoff) or you’re underwater (short sale territory).

- Whether you have additional liens, HOA issues, or title problems (common in distressed situations).

- How quickly can price, market, and close?

If you’re unsure where you are in the timeline, start by looking for the most recent notice you received and the recorded dates it mentions. LA County also provides consumer education on the foreclosure process and notices.

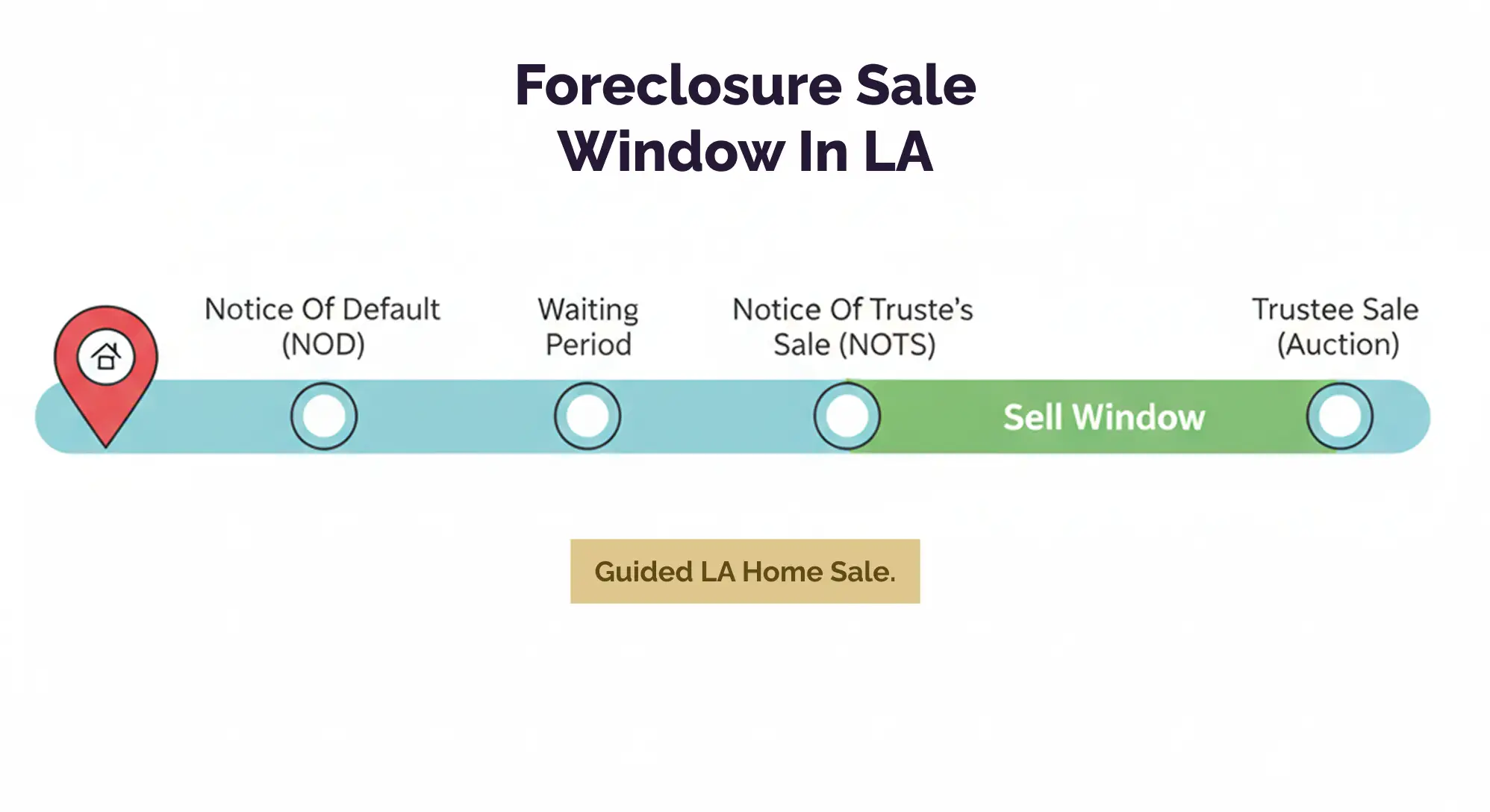

The California Foreclosure Timeline In Plain English

Most foreclosures in California are non-judicial, meaning they occur without a court case, but the lender must still follow a legally required notice timeline.

Here’s the simplified sequence homeowners usually experience.

Key Timeline Milestones (Typical Non-Judicial Process)

| Stage |

What It Means |

What You Can Still Do |

| Notice Of Default (NOD) Recorded |

Foreclosure becomes a formal public process |

Sell traditionally, pursue loan workout, plan a short sale if needed |

| Waiting Period After NOD |

A required window before the sale notice can be recorded |

Use this time to price correctly, prepare documents, and list |

| Notice Of Trustee’s Sale (NOTS) Recorded |

Auction is scheduled (sale date is coming) |

You can still sell, but time becomes the enemy |

| Trustee Sale (Auction) |

Home can be sold to highest bidder |

If sold at auction, your ownership can end (move fast well before this) |

California Courts’ self-help guidance describes the notice flow and the general timing: after required contact, a Notice of Default can be recorded, then later a Notice of Sale is recorded, and the trustee sale is set after required notice periods.

LA County’s consumer guidance also summarizes that if you don’t resolve the default, a Notice of Trustee Sale can be recorded, and it must be mailed and posted with advance notice.

Important practical point: if you wait until the sale notice stage, you can still sell, but you need a clean execution plan, a realistic price, and a buyer who can close quickly.

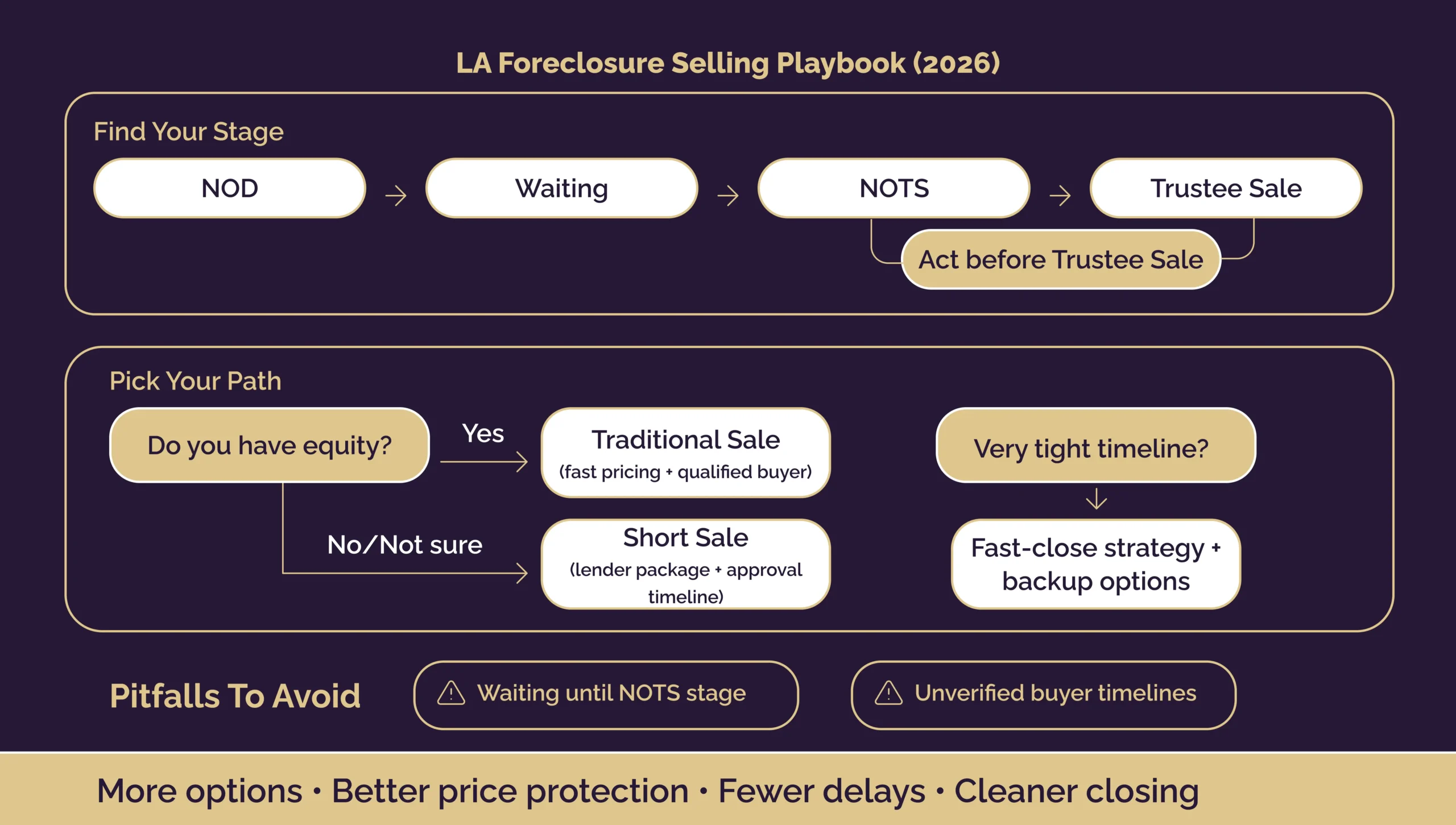

Your 3 Sale Paths: Equity Sale, Short Sale, Or Pre-Foreclosure Exit

Most Los Angeles foreclosure sellers fall into one of these three paths.

Path 1: You Have Equity (Traditional Sale Before Auction)

If your home can sell for more than what you owe (including fees and any liens), you can often do a normal sale.

What that looks like:

- List the home like a standard LA sale.

- Accept an offer with a timeline that beats the foreclosure sale date.

- Pay off the loan at closing, and foreclosure stops because the debt is paid.

This is usually the cleanest outcome if you have equity.

Path 2: You’re Underwater (Short Sale)

If your home is worth less than what you owe, your lender may need to approve a short sale. A short sale is a sale for less than the mortgage balance, and it’s considered a loss-mitigation option.

What changes in a short sale:

- The lender reviews your hardship and the offer.

- Approval takes time and documentation.

- Price expectations are shaped by the lender’s process and market reality.

Short sales are often still better than letting the property go to auction, but they require coordination and speed.

Path 3: You Can’t Sell In Time (Deed-In-Lieu Or Other Exit Options)

If a sale isn’t realistic, you may discuss alternatives like a deed-in-lieu of foreclosure, where you voluntarily transfer ownership to the lender to avoid the foreclosure process.

Also, if you’re overwhelmed or being pressured by “rescue” companies, use official resources first. California Courts warns about foreclosure rescue scams and points homeowners to HUD-approved counselors.

Selling With A Realtor In Los Angeles: What Changes

If your intent is transactional, selling with the right realtor is often less about “listing” and more about execution under deadlines.

A foreclosure-timeline sale has extra moving parts:

- Tracking the recorded notices and the sale date window

- Setting a price that actually produces offers quickly

- Managing disclosures and buyer concerns

- Coordinating payoff demands, lien checks, and escrow timelines

- If needed, guiding a short sale package and lender communication

TruLine positions itself as a “real estate and legal expertise” team, which can matter in complex transactions.

How To Sell A House With A Realtor In Los Angeles (Foreclosure Situation)

- Identify Your Stage

Confirm whether you’re at Notice of Default or Notice of Trustee’s Sale stage and what deadlines you’re facing.

- Run A Fast Equity And Liens Check

A strong agent will quickly estimate market value, net proceeds, and whether liens could block closing.

- Choose The Right Sale Strategy

Standard listing if you have equity.

Short sale if you’re underwater.

Backup plans if time is extremely tight.

- Price For Speed, Not Ego

In time-sensitive sales, pricing is the difference between “we got offers” and “we ran out of time.”

- Market To The Right Buyer Pool

Owner-occupants want condition clarity. Investors want margin. A good listing strategy filters time-wasters and targets closers.

- Create A Closing Timeline That Beats The Trustee Sale

Your escrow timeline must fit the foreclosure calendar, not the other way around.

Selling Without A Realtor: What You Must Handle Yourself

You can sell without a realtor, but foreclosure adds risk. The biggest danger isn’t just pricing wrong, it’s missing a deadline or mismanaging the payoff and title details.

If you go without a realtor, you need to personally manage:

- Pricing and comps in a shifting LA market

- Buyer screening (proof of funds or underwriting strength)

- Required disclosures and offer negotiation

- Escrow timelines and contingencies

- Payoff demand requests from your servicer

- Lien releases and title clearance

- If underwater, the entire short sale process and lender approvals

Also, be scam-aware. Government sources warn that foreclosure “rescue” operations may target homeowners in default. Stick to HUD-approved counseling resources and verified professionals.

With Vs Without A Realtor (Foreclosure Sale Comparison)

| Task |

With A Realtor |

Without A Realtor |

| Pricing and marketing |

Strategy + buyer access |

You do everything |

| Deadline tracking |

Agent helps manage timeline |

Easy to misjudge timing |

| Buyer qualification |

Pre-screening and negotiation |

You must verify everything |

| Short sale coordination |

Often guided and packaged |

You handle lender process |

| Risk management |

Experienced guidance |

Higher risk of errors |

Documents And Prep Checklist

The faster you can produce clean documentation, the faster you can close.

Seller Checklist (High Priority In Foreclosure Situations)

- Recent mortgage statement and servicer contact info

- Copies of any foreclosure notices received (NOD/NOTS)

- HOA documents (if applicable), dues status, special assessments

- Recent property tax status (especially if delinquent)

- Basic repair list and known defects (be honest, it prevents blowups)

- If pursuing short sale, hardship documentation required by lender

External resource suggestion:

If you’re unsure what a Notice of Trustee’s Sale looks like or how to read it, LA County has an explainer with sample elements.

How Buyers View Foreclosure Listings (And How To Protect Your Price)

Buyers typically assume one of three things when they hear “foreclosure”:

- The home is priced low because something is wrong

- The timeline is uncertain

- The transaction may be messy

Your job is to remove uncertainty.

How to do that:

- Be clear about the timeline and what stage you’re in

- Provide clean disclosures and documentation

- Price realistically, so you get decisive buyers quickly

- Don’t accept weak buyers who can’t close on time

This is where experienced LA agents earn their keep; they filter and negotiate under pressure.

If You Want To Buy A House That Is In Foreclosure (Quick Notes)

Since this is a common search alongside your main topic, here’s the practical answer.

Buying a foreclosure can mean:

- Buying before auction (pre-foreclosure sale)

- Buying at auction (often cash-heavy)

- Buying after foreclosure as an REO property owned by the bank

TruLine’s distressed property guide discusses foreclosures and REO basics for LA buyers and can be linked here as an internal resource.

If you’re buying, know that auctions can have different rules, and you may have limited ability to inspect or finance as you would with a traditional purchase. (For most homeowners reading this article, the priority is selling before it reaches that point.)

How To Choose The Best Real Estate Agents For Selling In Los Angeles (2026)

If your home is in foreclosure, you don’t just want “a good agent.” You want a plan, fast.

Questions to ask before you sign:

- How will you price for speed without giving away equity?

- What is your timeline strategy based on my current notice stage?

- What’s your plan if we need a short sale?

- Who handles payoff demands, title issues, and lien obstacles?

- What is the communication cadence (daily, every other day) until we’re under contract?

TruLine emphasizes heavy review volume and a mix of real estate plus legal background, which can be valuable in difficult transactions.

FAQs

Can I Sell My House If It Is In Foreclosure In California?

In many cases, yes, as long as the home hasn’t been sold at the trustee sale yet. The non-judicial process includes multiple notice stages, and many homeowners sell during that window.

Can I Sell After I Receive A Notice Of Default?

Often, yes. A Notice of Default is an early formal step, and it’s typically the best stage to act, because you still have time to list, market, and close.

What If I Already Have A Notice Of Trustee’s Sale?

You may still be able to sell, but you’re on a tighter timeline. You need a realistic price, a qualified buyer, and a closing plan that beats the scheduled sale date.

What Is A Short Sale And When Do I Need One?

A short sale is when the lender agrees to let you sell the home for less than the mortgage balance. It’s commonly needed when you’re underwater and can’t pay off the loan with sale proceeds.

Are There Free Resources If I’m Facing Foreclosure?

Yes. HUD offers resources for avoiding foreclosure, and HUD-approved housing counselors can help you understand options and communicate with your servicer.

How Do I Avoid Foreclosure Rescue Scams?

Be cautious of anyone promising guaranteed results for upfront fees. Government guidance warns about scam operations targeting homeowners in default and recommends HUD-approved counselors as a safer starting point.

How Do I Buy A House That Is In Foreclosure?

Foreclosure purchases can happen pre-auction, at auction, or as bank-owned REO afterward. Each path has different risks, inspection access, and financing realities.

Conclusion

Yes, you can often sell a Los Angeles home in foreclosure in 2026, but your success depends on acting early, choosing the right sale path, and timing your sale around the foreclosure timeline.

If you have equity, a standard sale before the trustee sale is usually the cleanest solution. If you’re underwater, a short sale may be necessary, but it requires lender approvals and strong coordination.

If you’re feeling pressured by “rescue” companies or confusing offers, use trusted resources first and get professional guidance.

Key takeaways:

- You can usually sell before the trustee sale; timing matters.

- A Notice of Default is the best time to act, as you have more runway.

- If you’re underwater, you may need a lender-approved short sale.

- Selling with an experienced LA agent helps manage deadlines, buyers, and payoff/title complications.

- Watch for foreclosure scams and use HUD-approved counseling resources when you need help.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}